Should You Charge Late Fees? QuickBooks Can Help

Many businesses struggle to pay bills these days, so it wouldn’t be surprising if your customers have been submitting payments later than usual these last several months. Still, you need to get paid – and on time – because delinquent receivables have a negative impact on your cash flow.

Ways to encourage prompt payment have been discussed in past columns. For example, you can start accepting credit/debit cards and direct bank transfers, make sure invoices go out immediately after a sale, or you can offer a premium like a small one-time discount for paying on time 12 months in a row. You can also assess finance charges on remittances that come in after the due date. QuickBooks provides the tools to allow this.

Setting It Up

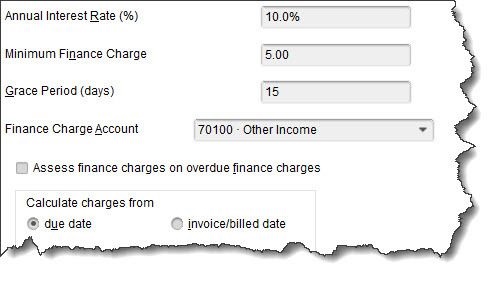

Before you start charging extra for late payments, however, you will need to do some setup work in QuickBooks. Open the Edit menu and select Preferences, then Finance Charge. Click the Company Preferences tab. You will see a window like this:

Figure 1: You can set your own preferences for assessing finance charges in QuickBooks.

You need to answer the following questions and enter your responses in the window:

What will your Annual Interest Rate (%) be?

What will you set as a Minimum Finance Charge?

Will you allow a Grace Period? A grace period is the number of days given to your customers to make their payments after the due date before finance charges kick in and is typically 15-21 days.

Where should captured finance charges go? In this example, the Finance Charge Account has been assigned to Other Income.

Do you want to Assess finance charges on overdue finance charges? Some jurisdictions don’t allow you to charge interest on overdue interest charges. If you want to do this, check on your local lending laws – specifically state usury laws, which may limit the amounts that can be charged.

When will you start to Calculate charges? In this example, the due date is selected. So, QuickBooks will start to add finance charges 21 days after the stated due date. If you choose invoice/billed date, you’ll want to make your grace period longer. This can be a confusing concept, so don’t hesitate to call if you want a deeper explanation.

Assessing Finance Charges

There is one more issue on the Preferences screen that you will need to resolve. QuickBooks offers two ways to notify customers about finance charges. You can’t include them on invoices the way you may be used to seeing them on credit card bills. Rather, you have to print separate invoices that only contain the finance charges. If you put a check in the box in front of Mark finance charge invoices “To be printed,” you can print them out separately. If you leave the box blank, the finance charges will appear on the customer’s next statement. Click OK when you’re done with this window.

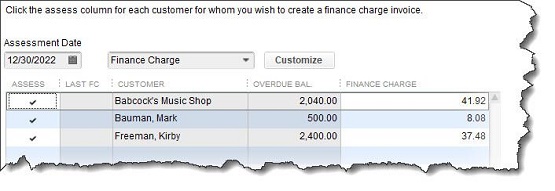

Figure 2: QuickBooks can find the overdue invoices that need to have finance charges applied and display them in a window like this one.

Open the Customers menu and select Assess Finance Charges. A window like the one in the image above will open. Make sure that the Assessment Date is the actual date you want to assess charges, which may not be the current date. Click in the Assess column to create a checkmark for every customer you want to charge. When you’re done, click Assess Charges.

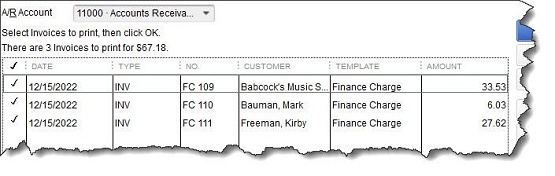

When you’re ready to print finance charge invoices, open the File menu and select Print Forms | Invoices to open a window like this:

Figure 3: Invoices with an FC preceding the number are finance charge invoices ready for printing.

Much to Learn

Besides knowing whether you can charge finance charges on existing finance charges, there are other considerations. For example, do your state’s lending laws allow you to use the phrase “finance charge,” or must you use something like “late fee?” When should you assess finance charges? Have you notified your customers of your intent to begin assessing finance charges? This is something they should know in advance, and you might need to add this to your customer message on invoices.

Finances charges may be the path you should take to improve your cash flow, but there are many issues to consider. If you need help with the mechanics of figuring this out, do not hesitate to call. Likewise, if you want to get started using this tool, please call.