Receiving Inventory With or Without Bills in QuickBooks

You’re probably happy to see couriers delivering inventory items you’ve ordered since it means you can ship to customers, but recording the new stock means yet

QuickBooks’ tools can help with this, but you need to be sure you’re using the right forms. There are two different ones that you’ll use, depending on whether or not you’ve received a bill.

Bill in Hand

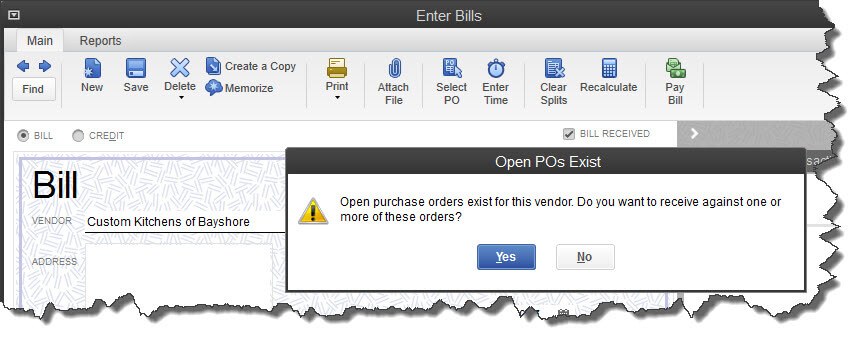

Either way, you’ll get started by opening the Vendors menu (or clicking the arrow next to Receive Inventory on the home page). If you do have a bill, select Receive Items and Enter Bill (Receive Inventory with Bill on the home page). The Enter Bills screen opens; select your vendor from the drop-down list. If you had entered a purchase order, you’ll see something like this:

Figure 1: If any purchase orders exist for that vendor in QuickBooks, you’ll see this message.

Click Yes. The Open Purchase Orders window will open displaying a list. Select the PO(s) for the items received by placing a check mark in front of it/them and click OK.

Tip: If you accidentally click No, the vendor’s information will be filled in on the Enter Bills screen, and you can click the Select PO icon in the toolbar.

Now the PO item information has been entered in the window. Check the form for accuracy, then save it.

Of course, if there was no purchase order, you’ll enter the information about the items you received (descriptions, prices, etc.) in the Enter Bills screen.

Delayed Billing

If you receive items without a bill, you still need to document the shipment. Open the Vendors menu and select Receive Items (or click the arrow next to the Receive Inventory icon on the home page and select Receive Inventory without Bill).

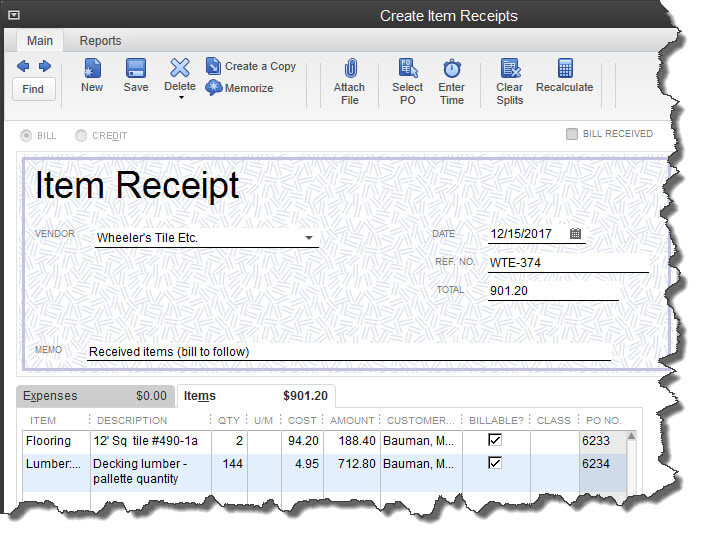

The Create Item Receipts window opens. Select the vendor by clicking the down arrow next to that field. If a message about existing purchase orders for that vendor appears, click Yes or No, and either select the appropriate POs or enter the information about what you received.

If the items were already earmarked for a specific customer on the purchase order, the Customer column will have an entry in it, and there will be a check mark in the Billable column. If there was no purchase order and you’re entering the information, you can complete those two fields manually.

Figure 2: If a purchase order was already assigned to a customer and is billable, that information should appear in this window.

Enter a reference number if you’d like. The Memo field should already be filled in with Received items (bill to follow), and the Bill Received box should not be checked.

Warning: Be sure that the Items tab is highlighted when you’re recording physical inventory. If there are related costs like freight charges or sales tax, click the Expenses tab and enter them there.

Paying Up

When the bill comes in for merchandise that you’ve already recorded on an Item Receipt, you’ll use this procedure to pay it:

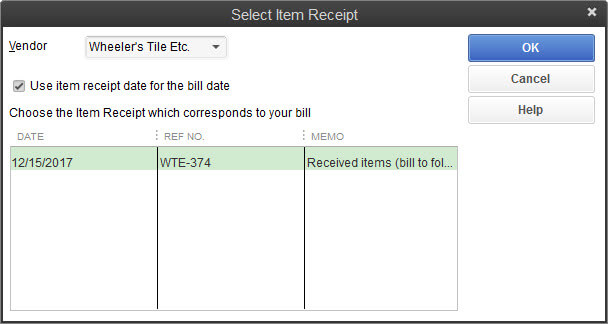

- Click Vendors | Enter Bill for Received Items, which opens the Select Item Receipt window.

- Select the vendor, then the correct Item Receipt.Note: If the bill corresponds to more than one Item Receipt, you’ll need to convert each into a bill separately. You can create a new bill if some items received were not accounted for on Item Receipts.

- Click the box next to Use the item receipt date for the bill date if you want to match it to the inventory availability date.

Figure 3: You’ll select purchase orders that you want to create bills for in this window. - Click OK. The Enter Bill screen opens, which can be processed like you’d handle any bill.

Though it may seem like extra work, this last procedure is important, since it prevents you from recording the same inventory items twice.

It’s easy to get tangled up on these procedures. We hope you’ll consult us when you begin implementing inventory management in QuickBooks, or when you’re taking on a new task there. It’s a lot easier to prevent errors than to go back and fix them.