Setting up Sales Tax in QuickBooks, Part 2

Last month, the focus was on the process of setting up sales taxes in QuickBooks. As you may recall, the first step is to go to Edit | Preferences | Sales Tax and make sure the software is set up correctly for this use. Before you do this, however, you will need to know what your state and local sales tax rules are. You can find this information on your state’s Department of Revenue or Department of Taxation website.

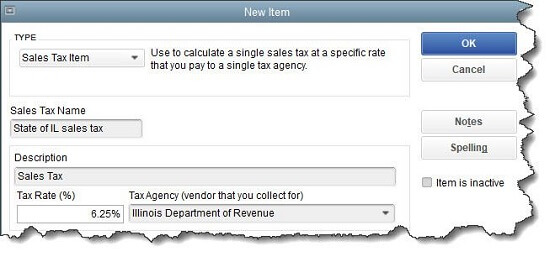

State sales taxes are considered Items in QuickBooks; you create them like you would create product records, and when local sales taxes are also required, you can set up Sales Tax Groups. You’ll be assigning these Items as well as Tax Codes to customers.

Using Sales Taxes

Once you have sales taxes set up, you can start using them in transactions. You can create them on the fly from within transactions, but we recommend taking care of this important housekeeping task before you start.

Figure 1: QuickBooks applies the Sales Tax Item or Sales Tax Group that you assigned to the customer on your invoices. You can see the others that are available.

Start by creating an invoice. When you reach the Tax column for your first line item, youâ??ll see that QuickBooks has already assigned Tax or Non to it based on the information in the item’s record. You can mix taxable and non-taxable items on the same invoice. You can also add a new sales tax on the fly from the invoice itself. Click the down arrow in the Tax column and select

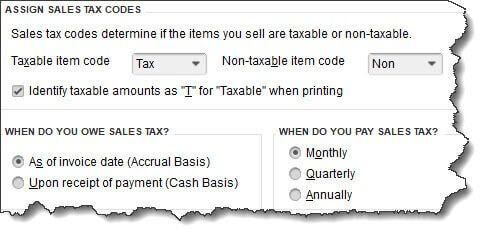

Be sure you’re not required to pay sales tax on an item when Non is selected. You may not have to charge sales tax on. For example:

- Nonprofit organizations

- Out-of state sales

- Items that your customers will resell

Tip: If you’d like, you can create more specific sales tax codes for these situations. You could use OOS for out-of-state sales, for example, LBR for labor, and NPO for nonprofit organization.

Figure 2: QuickBooks already includes Sales Tax Codes Tax and Non, but you can add additional ones that are more descriptive.

Be very careful with your sales tax classifications in QuickBooks. As was mentioned last month, such errors will be discovered in a sales tax audit, should you ever be subject to one.

Once you’ve entered all the line items in the invoice, look down toward the bottom of the screen, directly beneath the table containing invoiced items and above the Total. QuickBooks will have calculated the sales tax due using the Sales Tax Item or Group you assigned to that customer during setup, placing it in the Tax field.

Look to the left of those numbers, and you’ll see the actual rate that was applied. To the left of that is a drop-down list containing the correct Sales Tax Item or Sales Tax Group. Click the down arrow if you want to see the list of other options. And in the lower left of the screen, you’ll see the Customer Tax Code.

The Sales Tax Center

Figure 3: The Manage Sales Tax window.

When it’s time to pay sales taxes, you’ll open the Vendors menu and select Sales Tax | Manage Sales Tax. From the screen that opens, you’ll be able to:

- Access Sales Tax Preferences.

- Generate sales tax reports that help you fill out required forms.

- Visit related screens.

There are two reports you’ll need to run: Sales Tax Liability (displays total sales, amounts that are taxable and at what rates, taxes collected, and how much sales tax is due to each taxing agency) and the Sales Tax Revenue Summary (breaks down total sales into taxable and non-taxable). These reports are, of course, customizable, so you can filter them, for example, by Sales Tax Code.

A Delicate Balance

Collecting the correct amount of sales tax on taxable items and submitting the right tax totals to the right agencies takes vigilance. You don’t want to charge customers for unnecessary taxes, but you also don’t want to end up paying taxes you should have invoiced out of your own pocket. It’s much easier to spend a few minutes up front setting up sales tax accurately in QuickBooks than it is to go back and untangle inaccurate records. If you need assistance with this, don’t hesitate to call and set up a consultation.